Xerox – Cheap back to office play + Take private target?

Back to office will be a significant theme for the rest of the year and XRX is cheap way to play it.

XRX valuation in a hybrid work model

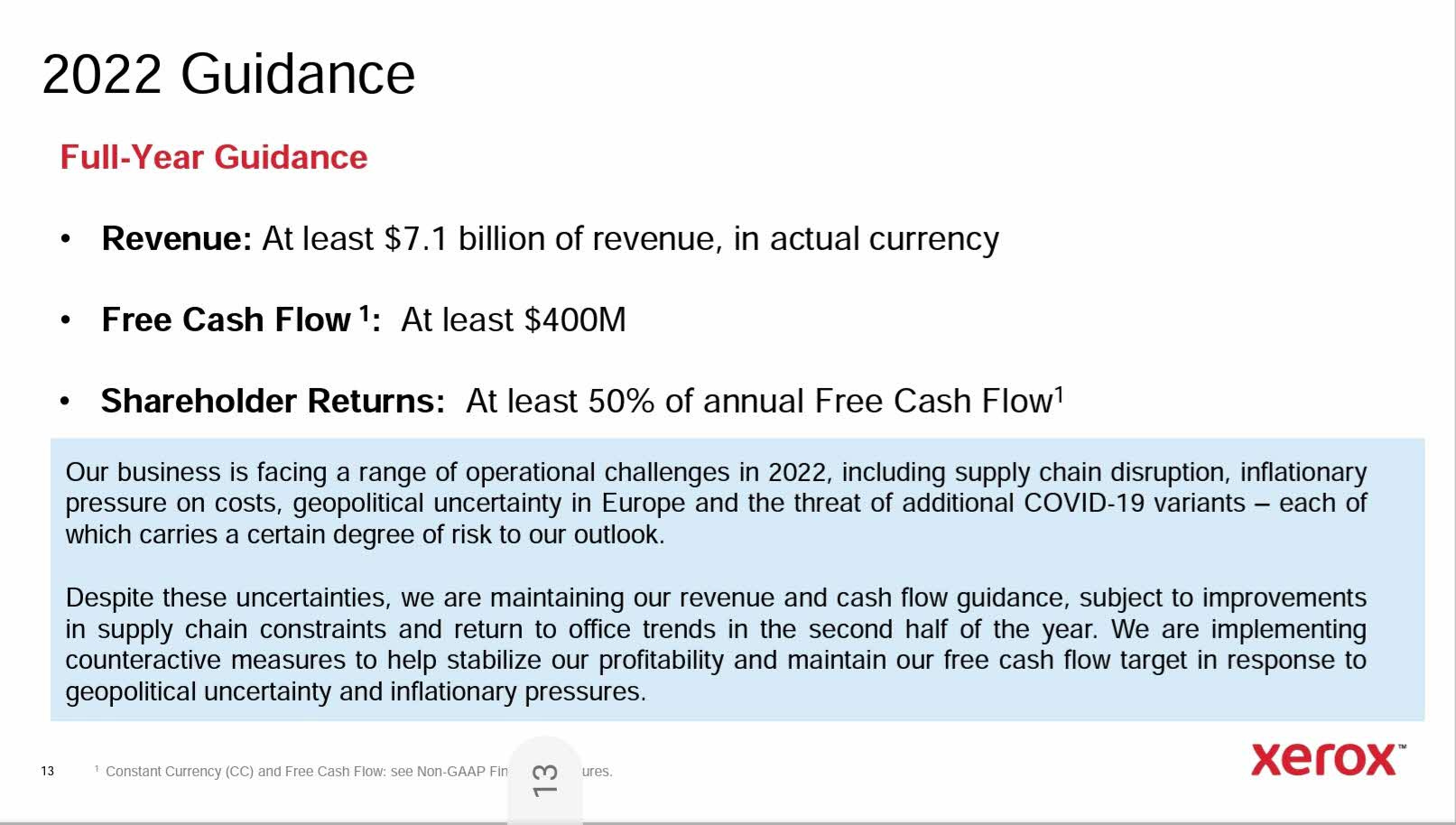

XRX free cash flow

Pre COVID years

2018 - $1.05bio

2019 - $1.27bio

Average - $1.16bio

COVID years

2020 - $0.47bio

2021- $0.56bio

Average - $0.515bio

Looking forward if the world settles into some sort of a hybrid work model, I expect XRX cash flow to be somewhere in between. Let’s use midpoint FCF of pre and covid year which works to $0.84bio.

At $0.84 bio free cash flow in a hybrid model, XRX is currently trading at Price to FCF of 3.2X.

Current valuation is half the valuation of what XRX traded right before covid. XRX traded at a price to FCF ratio of around 6.5X in 2019.

Take private target?

As XRX generated substantial cashflow during covid years it bought have aggressively at very attractive prices. Share count is down 27% since start of covid and continues to go down.

XRX policy is to return at least 50% of FCF. That translates to at least $200mio of dividends + buybacks in 2022. This is a very conservative as they have already returned $159mio (~6% of market cap) in Q1 alone (dividend $46mio + buyback $113mio).

Languishing stock price + aggressive buybacks has resulted in XRX market cap now lower than Q2 2020 COVID panic lows. I don’t think there is any back to office/reopening play out there trading lower than Q2 2020.

Carl Icahn is the largest shareholder of XRX with 22% ownership as he bought aggressively post covid selloff and continues to buy every post earnings selloff. The pace of buybacks seems to suggest management is in a rush to reduce share count. I won’t be surprised if Icahn offers to take XRX private in 2022 before back to office trends become clearer.

What does the EV chart look like?