Upstart: Easy Q1 beat & raise ahead?

Consumer loans macro environment remains constructive:

Loans Demand:

Consumer loans demand is accelerating. Q1 is seasonally a weak period for consumer loans due to tax returns. Seasonally total consumer loans outstanding peaks at year end. From there it falls till late March. It only makes a new high around July. This Q1 2022, consumer loans outstanding hardly fell from the peak and is already at a new high in late March.

Chart: Total US Consumer loans (not seasonally adjusted). Blue – 2022, Highlighted Green – Average of 2017,18,19,21.

The acceleration is clear in the seasonally adjusted series of total consumer loans below.

Subprime Loans performance:

Subprime delinquencies remain below pre covid levels in Mar despite inflationary pressures. KBRA Tier2 Marketplace Consumer Loan Index 30+ delinquencies stood at 3.4% in Mar 2022. Pre covid range was 4 to 4.5% for this subprime tier.

The index comprises of ABS deals backed by loans originated through Prosper, LendingClub, Upgrade and Upstart platforms and generally have weighted average FICO between 680 to 710.

Macro bottom-line:

Given accelerated demand, better than pre covid subprime performance & subprime ABS outstanding balance lower than peak, macro environment should remain supportive of subprime consumer ABS supply.

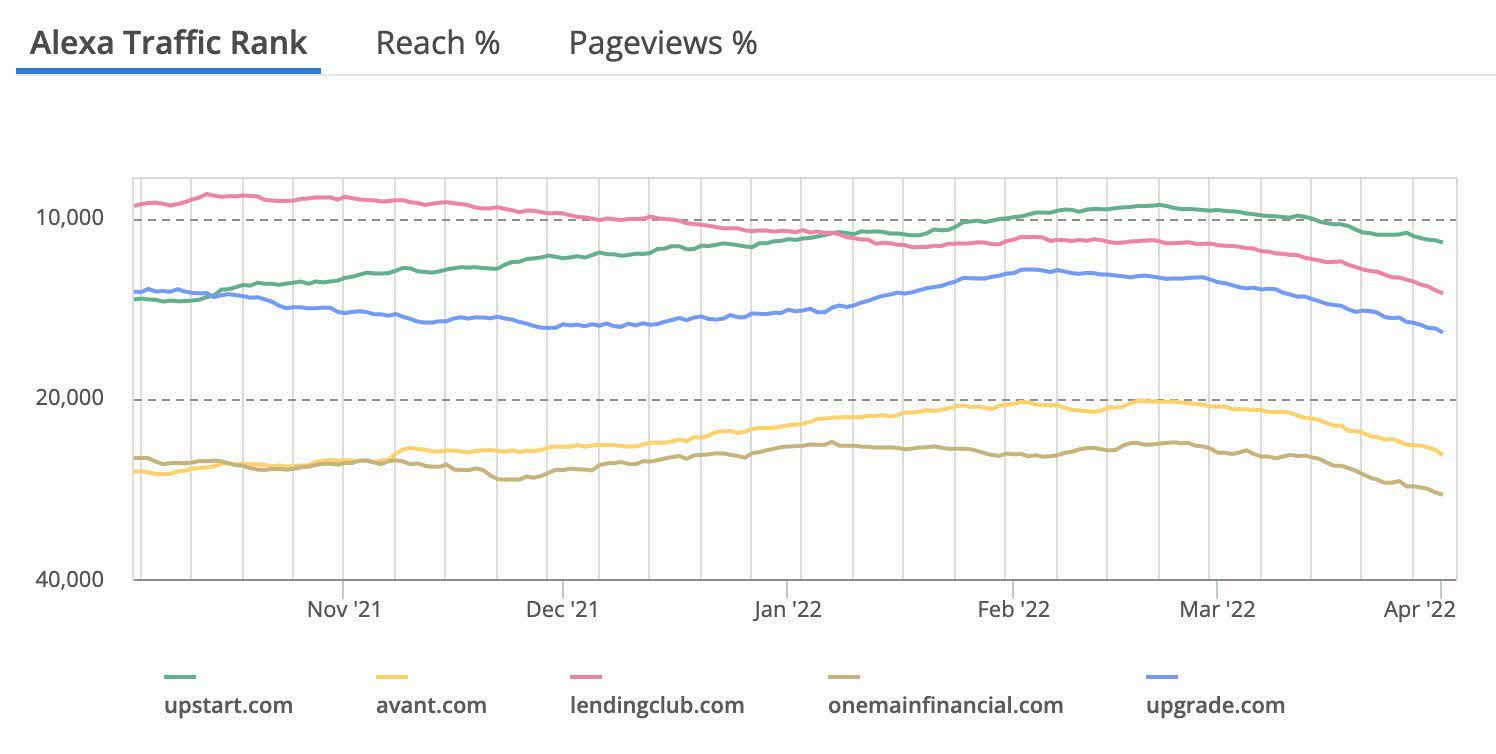

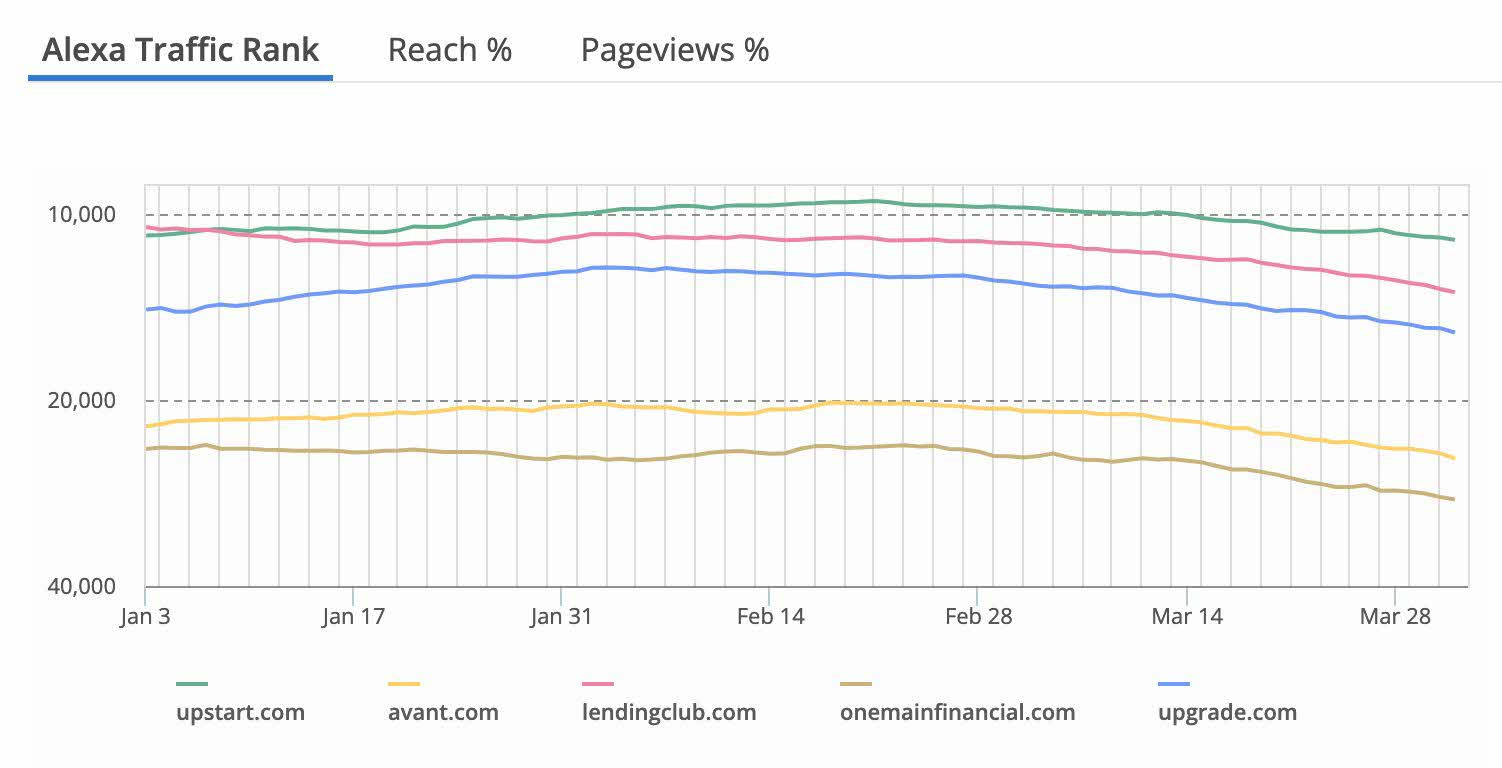

What about Upstart?

Upstart continues to gain market share from competition. In the past 6months, website traffic rank of upstart.com has gained past Upgrade.com and Lendingclub.com.

Upstart website traffic rank gained further in Q1 2022 implying more market share gains in Q1 2022.

Upstart.com actual website visits for Q1 2022 were 8.7million (vs 8.35 for Q4 2021) as per SimilarWeb data.

Upstart management guided a small sequential dip in revenue for Q1. Revenue guidance mid-point was $300mio for Q1 2022 vs $305 mio in Q4 2021. The reason stated was the seasonality of weak Q1.

But Q1 2022 has been anything but weak. Consumer loans demand has been much stronger than seasonal normal, upstart has continued to gain market share & website traffic grew sequentially. Considering these I expect Upstart to easily beat the guidance and estimates just like they did in Q4 2021. I also expect upstart to raise guidance given the strong macro environment & progress in the new auto purchase loans business.

Upstart risk?

One risk which has been highlighted for Upstart is the higher-than-normal delinquency seen late 2021 Upstart ABS issues. In my opinion this can be explained by the loan origination mix in Q3-Q4 2021. For the first time Tier C,D,E & F loans made up over 70% of loans in H2 2021.

KBRA also has the same view

I will be monitoring this closely and expect Upstart origination mix to tilt back toward better tier borrows going forward.