Pfizer: COVID beneficiary trading at pre COVID price

+45% to fair value

PFE trades exactly where it traded 1 year ago despite being the first to market on the COVID vaccine.

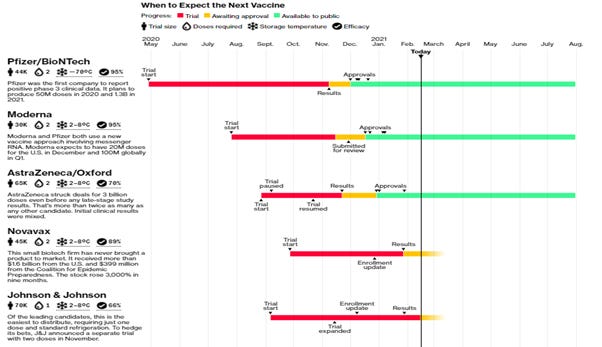

PFE COVID vaccine has the highest efficacy and PFE has the capacity to produce in scale. It plans to produce 1.3 billion doses in 2021. PFE already has contracts in place for ~1 billion of doses in public domain.

Source:

https://www.bloomberg.com/graphics/covid-vaccine-tracker-global-distribution/

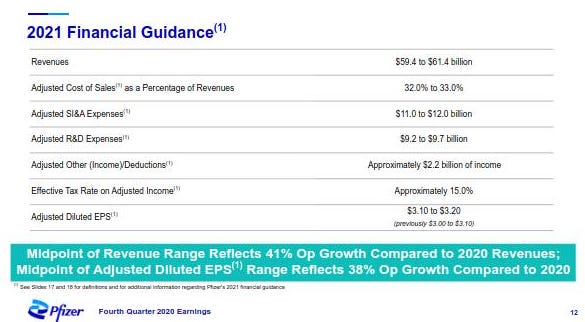

PFA has guided $15bio revenue at high 20s EBIT margin from COVID vaccine in 2021. PFE has guided overall 41%, 38% revenue and EPS growth for 2021.

The revenue growth doesn’t all come from COVID vaccine. Excluding COVID vaccine, PFE is guiding to grow revenue by 6% in 2021. PFE is also guiding 6% CARG revenue growth till 2025 excluding COVID vaccine.

So what multiple should PFE trade on 2021 EPS mid guidance of $3.15?

At current price of $34.7, PFE trades at 11X $3.15 2021 EPS & 15.3X 2020 EPS.

11X is cheapest multiple PFE has traded in the last 7 years. 15.3X trailing PE is cheaper than PFE median multiple in the past 7 years. No credit has been given to PFE for the COVID vaccine.

The median PE over the past 7 years is about 16x (chart below). In my opinion, 16X is a more appropriate multiple as some part of COVID vaccine revenue could be recurring & the 6% CAGR revenue growth outlook ex COVID vaccine.

At 16X $3.15 PFE should trade at $50.4 (+45% higher to current stock price).

Q1 & Q2 2021 should show strong growth from COVID vaccines sales.

PFE is COVID beneficiary trading at pre COVID stock price. PFE is a low risk situation with reasonable returns which should rerate fast.