Paysign asset lite, high growth COVID reopening value play

Paysign asset lite, high growth COVID reopening value play

Paysign provides payment solutions for the blood plasma collection industry. The below piece from Altafox capital has all you need to know about Paysign (then called 3PEA).

https://www.altafoxcapital.com/s/Alta-Fox-TPNL-Long-Idea-72418-xypk.pdf?fireglass_rsn=true

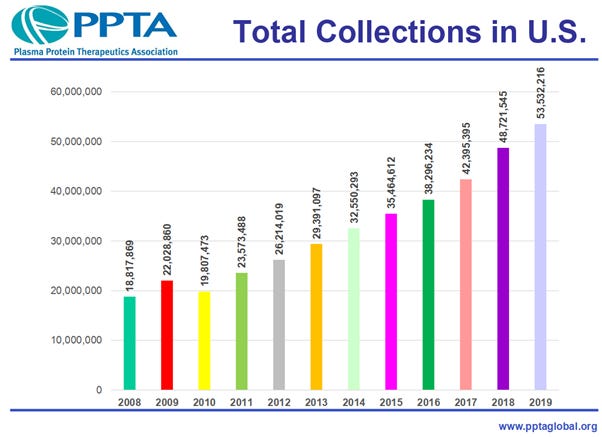

Plasma collections grew reliably over the years till 2019. COVID has hit plasma collection hard.

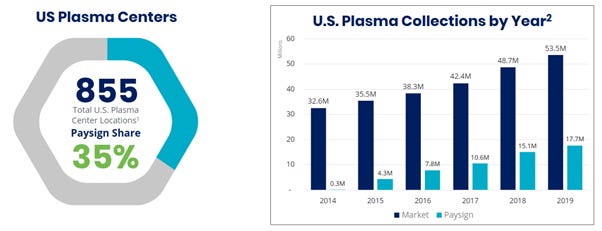

Paysign in addition to participating in the industry growth also captured market share from Wirecard. Paysign’s market share now stands at 35% from close to zero in 2014.

The combination of industry growth and market share growth resulted in 45% CAGR revenue growth for Paysign between 2016-2019. This kind of growth should resume in post COVID US.

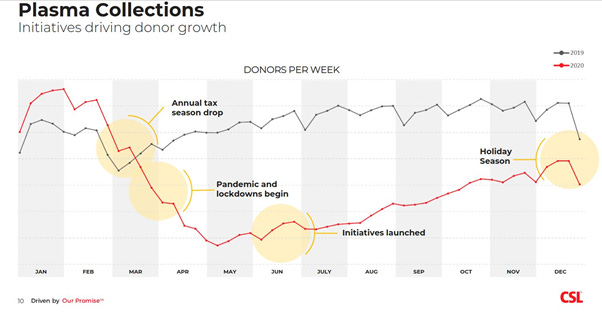

In 2020 COVID brought various headwinds to plasma collections including lock downs, reduced mobility of donors, social distancing restrictions etc. The below chart from CSL shows YOY donors per week. Collections went negative YOY in mid-March 2020, bottomed in about May and has been recovering ever since. December collection was only -20% YOY.

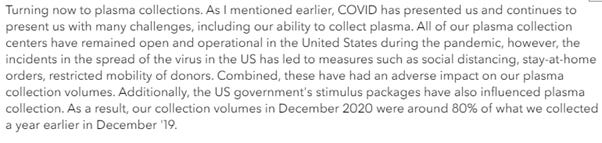

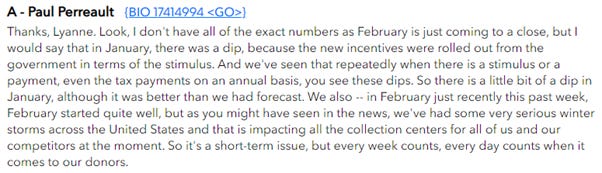

Extracts from CSL earning call on 18 Feb 2021 below. CSL also mentioned Jan was weaker than Dec on stimulus. Feb was strong till weather turned bad.

Other plasma collection players also speak about similar sequential improvements QoQ. Extracts from Takeda (via Shire) earnings call.

All signs point to the industry returning to BAU steady growth post COVID. I believe Paysign can grow at least at half its earlier growth rate at 22%. Even though 2020 revenue has been hit for Paysign, other drivers continue to grow.

While most stocks which would benefit from post COVID normalisation have rerated immensely, Paysign is at the lows.

Paysign is an asset lite, zero debt COVID reopening growth play trading at 14X T12 cash flow. Paysign should at least grow at 22% in a post COVID US.

Paysign is extremely cheap here. One reason for its cheapness could be the one-time accounting restatement last Q which makes it screen very badly. This should normalize with next Q results.

BTW, the excerpt from Paysign's investors' presentation with Business Drivers is bullshit. It took me some time to realize this. Note that the metric Funds Loaded on Cards is meaningless, because it's not "net" funds on cards but "Gross" funds ever loaded on cards (even though customers later withdraw funds). The total amount on cards is much lower and can be found on the BS (around $50M). Also, they don't show the number of active cardholders and the churn. A lot of window dressing on this slide on behalf of the management.

Also note, that operating cash flow almost entirely consists of funds loaded by cardholders. This money is not available freely to Paysign. Makes the valuation metric look impressive but it's meaningless.

Great write up! You and Run Rate PF Adj. EBITDA have turned me back onto this name big time. I'd urge you to look up the 2023 $5 Calls just as I did him, I think they are a fantastic and safe way to add leverage to the thesis.

Disclosure: Long 2023 $5 Calls