Lockheed Martin Corp (LMT) - no brainer buy?

LMT is a business with moat, with double digit EPS growth, trading at 11X PE with 3% dividend + 3% buyback yield

I just took a long position in LMT. It seems like a safe, easy money trade.

The below piece gives a good summary of LMT business lines as a background.

A quick look at the financials below:

LMT sales has grown mid to high single digit in the past with earning growing around 10%. EPS growth has been higher.

Can this growth continue?

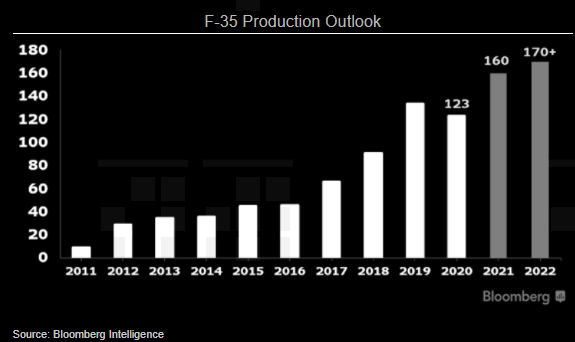

Yes. LMT backlog has been growing and now stands at the highest-level indicating sales growth ahead.

LMTs most recent outlook guides sales growth of +4% YOY for 2021.

Is it cheap?

Yes. LMT is trading at 11X T12 PE (red line in the chart).

Current valuation is around the cheapest in 7years and around the COVID panic valuation of Q1 2020.

Is management taking advantage of the low valuation?

Yes. LMT has accelerated buybacks in 2021. LMT has bought back $1.5bio of shares in H1 2021. This is higher than their rate in the past.

In addition to the buybacks, at current price LMT has a 3% dividend yield as well.

Bottom-line:

LMT is a business with moat, with double digit EPS growth, trading at 11X PE with 3% dividend + 3% buyback yield.

Sounds like a no brainer to me.