H&R Block Long Thesis $HRB

H&R Block (HRB) provides tax filing service.

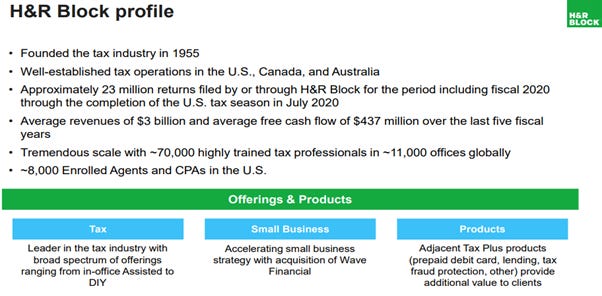

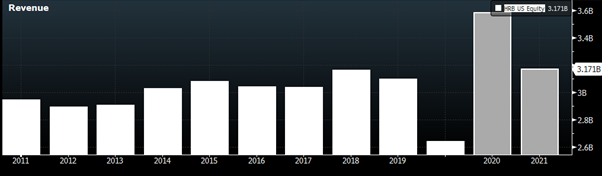

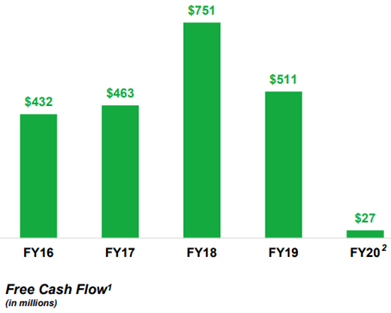

HRB doesn’t offer growth but is a stable business. The stock has traded cheap over the years and is extremely cheap right now. As the profile says HRB revenues has been stable at about USD 3bio and average FCF of USD 539 mio per year over FY 2016-2019. FY 2020 & 2021 is distorted due to extension of tax filing deadline due to COVID.

Current market cap is USD 2.84bio. Using the avg FCF of USD 539mio. P/FCF is 5.3X. Current dividend yield is 7% and they have resumed buybacks as well.

HRB is -37% YTD. Given the ytd performance one would think the business has been impacted severely by COVID. To the contrary there has been no impact.

Because of extension of tax filing deadline from HRB’s Q4 to Q1 the earning is distorted. A good way to view this is to add Q4+Q1 to eliminate the distortion.

Q4+Q1 2020-2021 (Covid impacted)

Revenue $2.401Bio

EPS $3.56

Q4+Q1 2019-2020

Revenue $2.45 Bio

EPS $3.6

The Q4+Q1 performance is basically flat YOY. There has been no impact due to COVID. This makes the -37% ytd an opportunity.

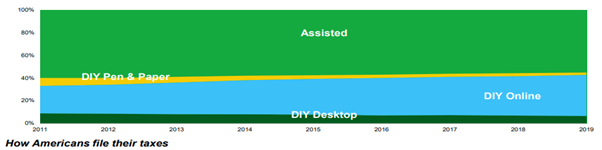

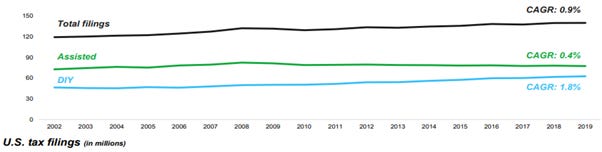

The long-term bear thesis seems to be switch from high margin assisted fillings to low margin DIY fillings. But the switch is pretty slow and assisted is still growing. In the latest US tax season HRB saw +3.3% yoy increase in filings signalling increased market share.

HRB is very cheap. It’s a stable business trading at 5.3X P/FCF. Ytd selloff is unjustified given no impact due to COVID. The bear thesis is invalidated as even COVID didn’t hurt assisted fillings much. 7% dividend yield + buyback should lead to rerating. Recent insider purchases validate value.